Numerous trends are driving the short-term and long-term demand for gas globally.

These include, but are not limited to, decarbonisation efforts by numerous countries around the world and the sanctions placed on Russia’s gas due to its war with Ukraine. In turn, capex on new LNG capacity—both liquefaction and regasification—has skyrocketed over the past several years, with hundreds of billions of dollars in announced investments under development globally.

As global gas consumption is set to significantly increase, LNG demand is forecast to more than double, to 800mn t/yr by 2050, according to the Gas Exporting Countries Forum (GECF). LNG regasification terminal capacity is forecast to increase from nearly 950mn t/yr in 2020 to nearly 1.57bn t/yr in 2050. However, with a finite amount of LNG available globally, prices are expected to increase, especially for Asian markets as China has now re-entered the scene. For example, Morgan Stanley has increased its price outlook on Asian LNG pricing for 2023 and 2024.

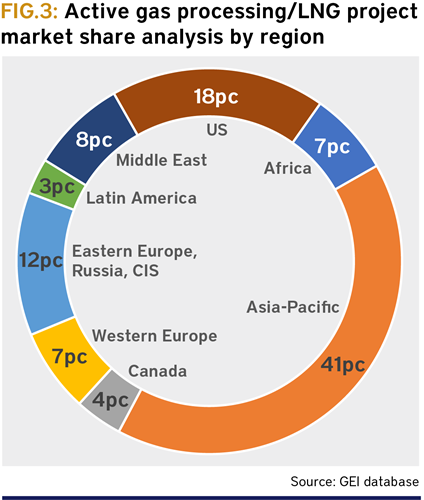

According to the GECF, global gas demand will continue to increase until 2050. The forum’s report, Global Gas Outlook 2050, sees demand surging to more than 5,600bn m³/yr by 2050. Nearly 50pc of the demand growth will come from the Asia-Pacific region, which is investing heavily in additional infrastructure to limit carbon emissions—a major driver of the region’s gas demand comes from switching from coal-fired power generation to gas. Global Energy Infrastructure, the market intelligence platform by Gulf Energy Information that tracks LNG/gas processing projects worldwide, demonstrates this point perfectly. At the time of publication, of nearly 240 active projects, 100 alone are in the Asia-Pacific region awarding them the highest market share.