Europe’s LNG imports increased by 75pc year-on-year to a total volume of more 108bn m³, or 22pc of the continent’s gas consumption, according to the European Commission’s most recent quarterly report on gas markets.

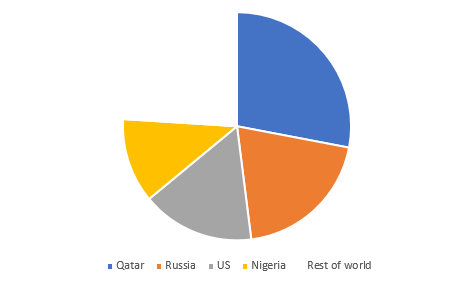

Qatar retained its traditional slot as the largest LNG supplier to Europe by country, but relatively new entrants Russia and the US rose to second and third, respectively (see Figure 1) .

Figure1: Qatar retains European LNG lead

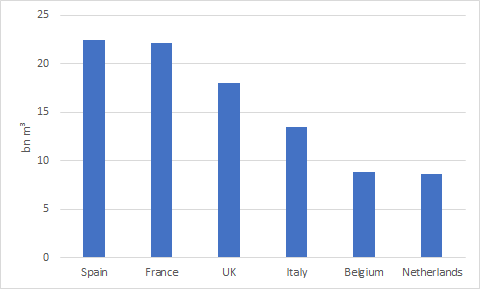

Similarly, Spain and France remained, as usual, heavy imports among the EU-28, but the UK—which receives virtually all of its deliveries on a spot, rather than contractual basis and can, in a very tight supply year, receive only a bare minimum of cargoes required to keep its facilities cool—jumped to third (see Figure 2).

Figure 2: UK joins Europe's LNG import big league

In 2019, EU-28 gas consumption increased by 2pc year-on-year to reach 482bn m³. But this year looks very different. Demand may be set to contract sharply amid the recessionary environment. And benchmark TTF prices are at record lows, thus reducing margins for LNG exporters shipping cargoes to Europe.

In the competing demand centre of Asia, demand and prices are also under pressure, Asia’s price premium over Europe is only around the increased logistical costs of shipping gas there. Moreover, Europe has around 100bn m³ of storage capacity, which allows for greater flexibility to accept volumes compared to more storage-constrained Asian countries.

"Europe has something Asian markets do not have—storage facilities and access to liquid hubs. There is huge storage space in Europe compared with Japan and South Korea; this is a point that is often overlooked," Greg Molnar, a Paris-based gas analyst with the International Energy Agency (IEA) tells Petroleum Economist.

On the other hand, Europe’s storage may be filled by August or September. The continent’s storage facilities are already c.60pc full on average at an unprecedently early point in the summer injection cycle—although that figure excludes Ukraine’s 31bn m³ of capacity which may offer some additional injection potential this summer.

Domestic decline

Even with potential demand and storage headaches, Europe’s dropping indigenous production continues to be a boon for its gas importers. Output from the giant Groningen field in the Netherlands is set to be almost fully phased out by 2022 on the back of government legislation after a series of earthquakes damaged property sitting above the onshore field.

Despite the North Sea’s mini renaissance between the 2014 and 2020 price shocks, UK production from ageing fields continues to fall. Any growth in Norwegian volumes expected to flatten out by 2023-24. And its largest producer, Equinor, is expected to continue to pursue its long-standing ‘value over volume’ strategy which has seen production from the giant Troll swing field regularly undershoot permitted output caps since the global gas market swung decisively toward oversupply more than a year ago.

However, there are limits to the potential upside from declining indigenous production. Europe’s import dependency already stands at over 80pc of consumption. Therefore, the continent’s demand growth, or lack thereof, will also be key to LNG’s prospects.

Demand questions

European industrial and commercial (I&C) gas demand has already been and will continue to be severely impacted by Covid-19, and any recovery and future demand growth will depend on the speed of economic recovery. While European policy makers largely see gas as a key fuel to partner the renewables boom and transition to a greener economy—although there is a small but vocal, and possibly growing, anti-gas lobby in Brussels—this will have only a medium-to-longer-term impact on demand

Shorter-term, Europe’s 2019 gas demand growth was led by fuel switching in power generation, owing to relatively high prices for EU carbon allowances and lower gas prices relative to coal. But the more coal is squeezed out of the European power mix, the more limited the scope of further fuel switching.

A drop in coal demand also helps to push down prices both for that fuel globally and for European CO2, due to lower emissions. Covid-19 will also depress both these markets, meaning ever lower required gas prices to outcompete what coal-fired capacity is left to switch

LNG versus pipe

LNG suppliers’ hopes that Europe can absorb yet more of their gas in 2020 may thus depend on LNG outcompeting pipeline gas. Russia—which supplied almost 50pc of Europe’s gas imports in 2019 including both LNG and pipeline gas—provides an interesting case study

Volumes of Russian pipeline imports may decline in the first quarter of 2020. And it is not clear to what extent state-controlled gas heavyweight Gazprom is committed to using its 32.9bn m³/yr Yamal-Europe pipeline going forward, given the transit contract on the Polish section of the pipeline is due to expire this spring. That said, it settled a much trickier transit renewal with Ukraine at the end of last year with relatively little fuss.

Lower oil prices threaten to put a fly in LNG’s ointment, although not for the reasons it once might. “Oil-indexed contracts might become more cost competitive once lower oil prices filter through the formula. However, this will more impact Asian markets, as in Europe there is not much oil-indexation left,” says Molnar.

Norwegian supply is almost entirely on gas-to-gas pricing, while Gazprom’s pipeline contracts, at least to destinations with supply diversity, also contain substantially less oil linkage than in the past.

North African pipeline, and indeed contractual LNG, supply may be more relevant—Algeria’s Sonatrach has remained, at least publicly, a stubborn champion of the traditional oil link in its gas pricing. It remains unclear if it was able to face down customers more sceptical of oil’s continuing gas price relevance in contract renewal discussions, but, if so, spot LNG may find tough competition in southern European markets.

But lower oil prices also make it cheaper for Gazprom to export pipeline gas. This is because the oil price is one of the components used when calculating Gazprom’s export duty and production taxes—alongside the RUB/USD exchange rate and gas sales prices in Europe.

“Overall this gives Gazprom a more comfortable position to weather low prices. Importantly, Gazprom’s short-run marginal cost appears to be below that of US LNG for now,” says Oleg Vukmanovic, a gas and LNG analyst at consultancy Poten & Partners—although cautioning the Henry Hub volatility could swiftly reverse US LNG’s disadvantage.

Even very incremental European LNG markets face pipeline gas battles. In southeast Europe, the EU-backed 2.6bn m³/yr Krk terminal in Croatia is slated for early 2021 completion. But, in

the same region, there is the 10bn m³/yr TAP pipeline linking Europe with Azerbaijan, which also has EU support, and Russia’s Turksteam (15.75bn mە/yr to Europe), with which it must contend.

Poland has had an appetite for Qatari and S contractual LNG as a supply diversification play away from Russian gas. But the new 10 bn m³/yr Baltic Pipe, bringing it Norwegian gas via Denmark is expected to be operational by October 2022.

LNG imports cannot expect to find European demand as of right. In the current environment, finding it at all could be an achievement.

Comments