Future oil demand growth lies in the east, as oil consumption has already peaked in Europe and the US. China and India, with their large populations and burgeoning economies, are central to the global oil demand outlook.

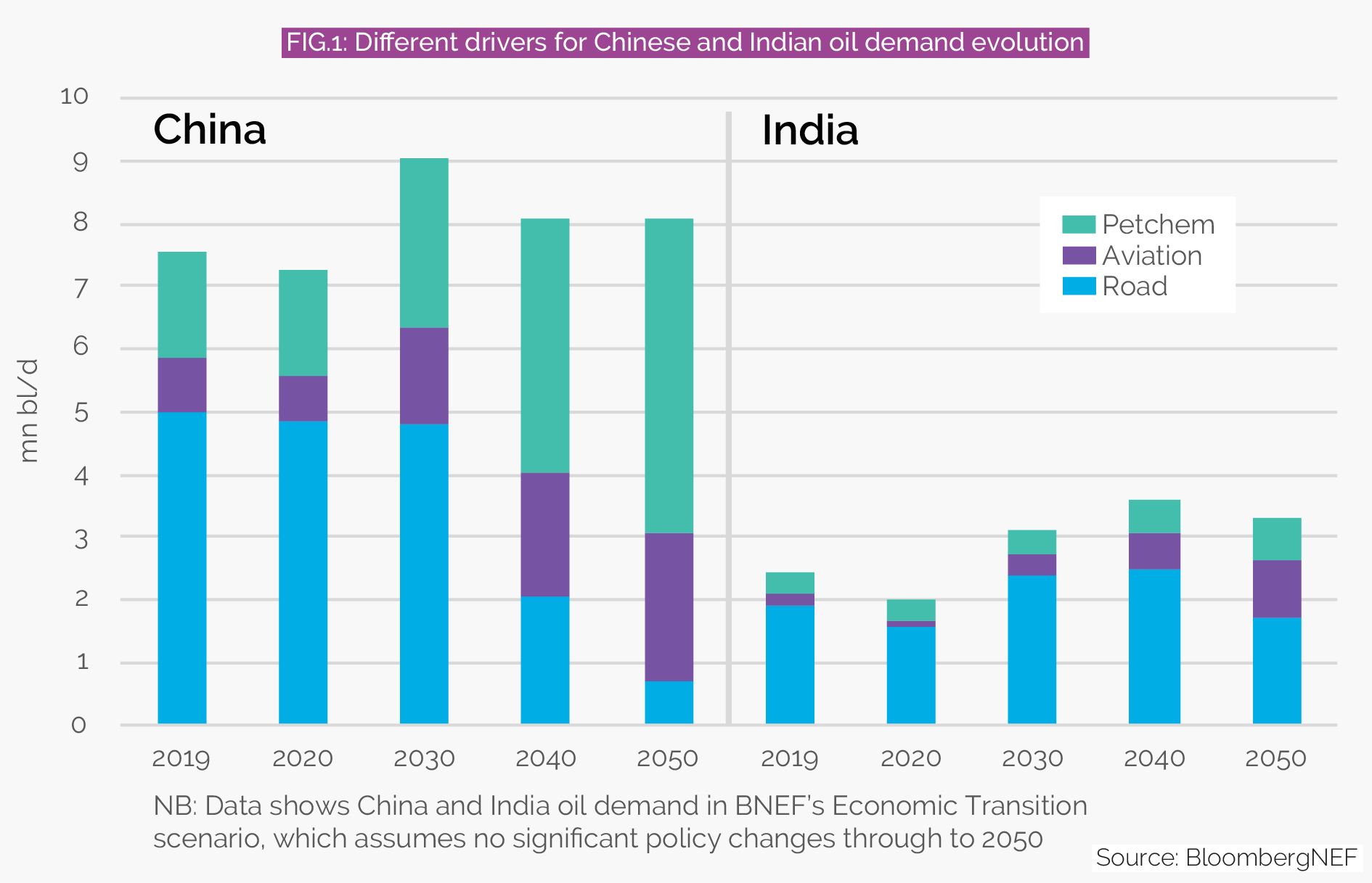

Both countries will continue to see oil consumption rise before peaking, but—according to BloombergNEF’s Economic Transition scenario, which assumes no significant policy changes through to 2050—the composition of their future barrels will be quite different (see Fig.1), making adaptation vital for survival and success in the sector.

Prosperity-led growth

The ever-increasing need to move people and goods around will be the biggest driver of India’s oil growth. The world’s second-most populous nation will become one of the fastest-growing markets for passenger vehicles by 2050. India’s demand for freight movement almost triples by that date, making it the largest market in the world.

Electric vehicles (EVs), the major threat to road fuels, penetrate slowly into India’s booming transportation sector. Passenger EVs take off after 2030 as they become more cost-efficient than internal combustion cars. Commercial EVs, on the other hand, need to further overcome infrastructure constraints in their competition with fossil-based trucks.

Slower uptake of EVs supports India’s consumption of gasoline and diesel in the coming decade. Road fuel demand increases by 40pc before peaking around the mid-2030s. It then falls back to current levels by the middle of the century.

India’s air travel also grows at a higher rate than most other countries. With such a large population, a small increase in air travel propensity translates into a significant boost to jet fuel demand. India’s jet demand recovers to pre-pandemic levels in 2023 and increases fivefold by 2050, to 900,000bl/d.

Population and income growth are likely to drive continued expansion for plastics, pushing up demand for petrochemical feedstocks. India’s oil consumption in the petrochemical segment is set to double by 2050 on the back of increased wealth and economic growth.

China in transition

China’s appetite for crude has more than tripled since 2000. Following its entry into the World Trade Organization and an era of economic boom, China became the growth engine for oil demand in the past two decades. However, over the next 30 years, China’s oil demand evolution is likely to decouple from its economic growth rate, a fundamental shift that is unprecedented in previous playbooks.

The biggest challenge comes from road fuels. Government subsidies and policy support have paved the way for early penetration of EVs into China’s automobile market, leading to a flatlined oil demand curve from the sector during the 2020s, despite an increasing need for road transport. Demand disruption becomes more prominent after 2030, as the uptake of alternative drive trains also helps erode 4mn bl/d of oil demand by 2050, or nearly 90pc of China’s current road fuel consumption.

Losing 90pc of their biggest revenue stream, and arguably the biggest profit pool, leaves Chinese refiners struggling. They must find outlets before their assets become stranded. The aviation sector offers one way out—the underlying growth factors in China’s jet fuel demand are no different to those of India, although its comprehensive domestic rail network could limit the upside in jet fuel growth.

Petrochemicals offers another lifeline. China’s demand for petrochemical feedstocks more than doubles by 2050, making oil refining and petchems integration a popular option among traditional refiners and new entrants. Newly built mega-refineries yield over 60pc petchems—four times higher than the country average.

Existing refineries also look to retrofit to be more petrochemical-oriented. Petchems production becomes more attractive amid China’s green push as embedded carbon lowers the emissions intensity in end-products.

Adapting to the future

The oil industries in China and India may face divergent demand outlooks, but the need to evolve is something both countries have in common. Disruptive technologies, stringent policies and net-zero targets are changing the business cases for many stakeholders in the oil sector, forcing them to transform and convert.

With peak oil demand looming for both nations, the next billion-dollar question in the oil sector is not “where should I build my next mega-refinery?” but rather “how can I adapt to the ever-changing landscape?” Consumer preference might differ from time to time and from country to country, but pursuit of affordable, reliable and sustainable energy will persist. Oil players will need to be flexible to navigate and flourish through the energy transition.

Sisi Tang is an oil analyst at the strategic research company, BloombergNEF.

This article is part of our special Outlook 2023 report, which features predictions and expectations from the energy industry on key trends in the year ahead. Click here to read the full report.

Comments