With the world in the middle of an energy crisis, crude oil stands out as a comparatively cheap fuel versus fossil alternatives, even at some $90/bl. The problem is that most oil consumers are exposed to the wholesale price of refined products.

Of particular importance to both consumers and businesses is the price of diesel. In recent weeks, diesel has at times been pushing towards $170/bl, an $80/bl premium to the cost of the raw material and some five times the average historical premium of c.$15/bl.

At any other time, this would already be a clear reason to adjust oil demand expectations. This winter, it is an almost catastrophic price signal, with the global cost-of-living crisis already set to worsen over the next few quarters. Gas prices, electricity costs, mortgage payments, food costs and rising unemployment look certain to be a massive challenge for both populations and governments.

European authorities have done their best to shield populations from the rally in energy, but this is only a part of a wider picture of pressure on the consumer and business activity. What is more, outside of Europe, such protective measures are a rarity.

(Re-)enter China

The good news for consumers is that some of the factors behind the disconnect between diesel and crude prices look likely to change in the coming months. The first relates to China, where authorities over the past year had cut off its very large domestic refining industry from access to international markets. By now, very large export margins—and perhaps even a broader attempt to support both the global and Chinese economy—have seen this policy reversed, at least for the next few quarters.

That means a large volume of diesel from China is now expected back on the market. The surge may be independent of the country’s zero-Covid policy, or even boosted by it owing to weaker domestic demand.

The second issue is Russia, another large diesel exporter, particularly to Europe. Even the expectation that Russian flows may be cut off from the global market has allowed diesel prices to be sustained at high levels. What are the expectations for Russian oil flows following implementation of European sanctions on Russian crude, with refined products sanctions due to start in February?

One notable trend has been the gradual reduction in ambition from the G7 and its allies regarding Russian energy over the last few months. This is clearly related to the wider economic difficulties facing the world: the risks to energy security and economic activity are simply becoming too great to chase Russian oil with the vigour that many envision. What is more, market opinion is beginning to converge on the notion that the global fleet of tankers and insurers available to move Russian barrels may already be enough to skirt currently planned sanctions in the first place.

This notion may well need revising in the coming months, depending on the geopolitical situation. However, at present it appears as though we can expect more Russian oil to flow next year than previously expected. This will help to reduce the risk premiums expressed in crude and, in particular, diesel prices.

Let us, though, suppose the opposite situation, i.e., strict energy sanctions and/or unilateral cuts to oil flows from the Russian side. What would be the impact? Crude and diesel prices are likely to rise from currently already elevated levels at least initially.

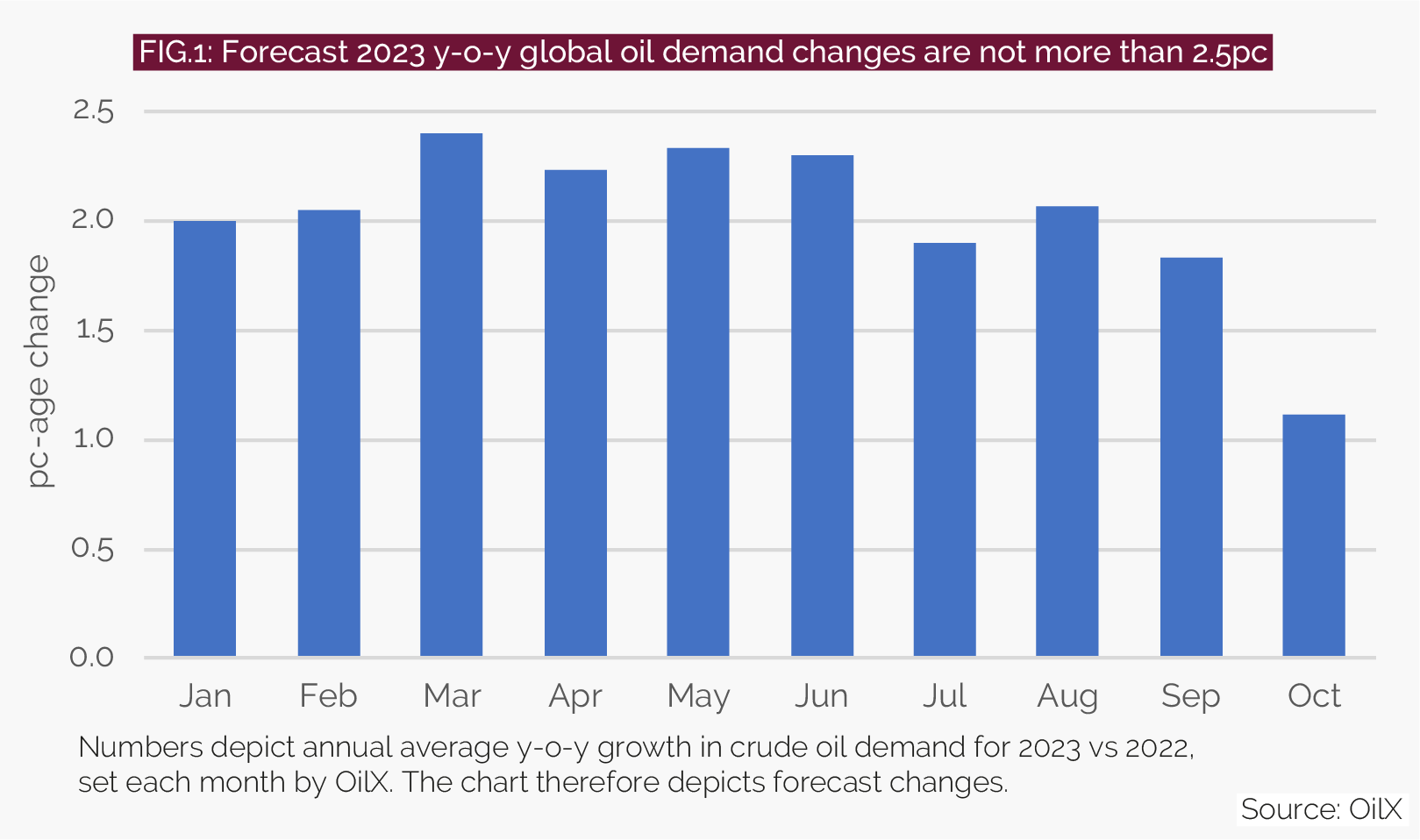

However, the history of high oil prices and economic crises suggest such price hikes tend to be self-defeating. There is already mounting evidence of weakening oil demand in both Europe and the US; further price volatility in this economic environment is only likely to further suppress demand—growth of which is already forecast to be relatively anaemic in 2023 (see Fig.1)—in the OECD and in emerging markets. Ultimately, this means that oil prices will eventually deflate once the extent of the damage begins to make itself clear.

The good news from the producer perspective is that there are clearly limits to how low prices can go. For diesel, another policy reversal in China may happen as soon as export margins dwindle, with long-term climate goals still in play. Moreover, spare refining capacity outside of China is more limited than before Covid.

For crude, the Opec+ group of producers has clearly signalled a desire to defend prices over the next year. It largely has a free hand to do so, with US shale now much less dynamic in terms of growth even at high prices, but still vulnerable to low prices.

Neil Crosby is a senior analyst at the oil analytics company, OilX.

This article is part of our special Outlook 2023 report, which features predictions and expectations from the energy industry on key trends in the year ahead. Click here to read the full report.

Comments