Let us start with the energy mix: how it is changing and why. The world’s population is projected to increase from close to 8b people to about 10b by 2050. Rapid urbanisation will drive around 70% of people into cities, particularly in Asia and Africa, and the global economy will double in size to more than $200t.

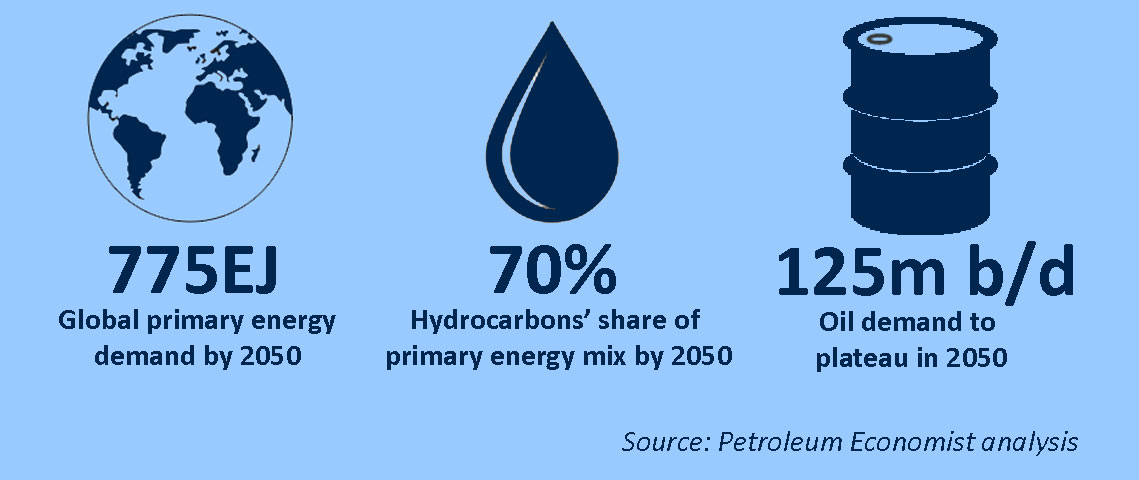

By 2050, global primary energy demand will increase by 25%, with Asia-Pacific and Africa leading the growth. As developing economies expand, urbanise and industrialise, energy consumption will continue to rise. Petroleum Economist sees primary energy demand growing from 635EJ in 2023 to 775EJ by 2050. Asia-Pacific is set to dominate global energy demand growth, contributing 70EJ, followed by Africa, while Europe should continue its gradual decline.

There are three key factors shaping energy demand: first, growth in petrochemicals, which is heavily linked to industrialisation and urbanisation; second, electrification, especially around air conditioning and heat pumps, electric vehicles and AI growth; and third, a slower, more challenging energy transition, given stubbornly high costs and long-term supply issues around potential replacements for oil and gas.

To meet that expected demand shift, China in particular is adding large petrochemical capacity. The key question is whether the world needs all this capacity or increased recycling and lower demand for plastics will take care of that. These additions could also lead to some rationalisation, with plant shutdowns possible in Europe and probable in Northeast Asia.

Electricity demand is coming from higher cooling demand in developing countries due to increasing temperatures, increased use of heat pumps, rising EV sales and electricity consumption by datacentres. The question is whether new chips will be able to reduce power consumption. Even with greater efficiencies, the growth in energy use is unlikely to be offset and thus that higher electricity supply will need to come from nuclear sources in the longer term or natural gas at least in the near-to-medium term.

A focus on costs, policy inertia and the need to pursue profitability with effective carbon management strategies in place will lead to a slower energy transition, as many project, and even slower than a business-as-usual case that may well lead to higher oil and—in particular— gas demand, at least for the next decade or two.

Most of the oil and gas supply in the next 10–15 years could come from the Americas. Guyana, the US, Canada, Brazil and Argentina will be the key suppliers. Similarly, Saudi Arabia, the UAE, Kuwait and Qatar will be key oil and gas producers in the Middle East.

Prices will play a pivotal role: a toxic scenario is if these prices are not adequate to support higher production and not low enough to hamper a shift to clean energy sources. This trade-off could be critical without the right policy frameworks, ones that kill or prioritise certain energy sources.

For Petroleum Economist, hydrocarbons are expected to remain dominant in the global primary energy mix, contributing 70% by 2050, down from around 80% in 2023. Natural gas, which accounts for 23% of global primary energy demand, is forecast to rise to 30% by 2050.

Renewables are the fastest-growing energy source, with their share projected to increase from 3% in 2023 to more than 20% by mid-century. Oil demand is anticipated to see a prolonged plateau after 2035 at around 30% of the energy mix. Coal’s share is anticipated to collapse, from 27% to just 10% over the outlook period.

Nuclear and hydrogen will continue to struggle to make inroads into the primary energy mix given present policies and prices, although some circles still believe a dip in hydrogen production and storage costs, along with the development of infrastructure with the help of governmental policies, could make it a viable energy source.

Oil

Petroleum Economist highlights the essential role of energy in meeting humanity's needs, pointing out its importance in heating, cooling and enabling modern conveniences. According to the UN, 1.18b of the world’s population is in energy poverty—i.e., below the modern energy minimum of 50m Btu/yr.

According to ExxonMobil, around 160m Btu/yr of energy is consumed in developed world. To provide the whole world with additional energy, more production sources are needed, including hydrocarbons. Petroleum Economist projects a 35% rise in energy consumption in developing nations by 2050, which will be mitigated by a 10% fall in energy use in the developed world thanks to efficiency gains: making that a 25% net rise in energy consumption.

Oil and gas are part and parcel of this energy mix. Petroleum Economist’s outlook foresees oil and gas making up 60% of the world’s energy mix in 2050, higher than the 56% seen in 2023, while its absolute use will also be higher. This is in contrast with many bullish oil and gas scenarios, which still see a fall or plateau but may well be revised higher in their new additions after what we have seen in the past six months across oil and gas companies and policymakers, especially in the US.

Petroleum Economist agrees with some other views about continuous oil demand growth. Despite growing alternatives—including electric cars—oil and gas will still be required in 25 years from now. ExxonMobil gives this salient example: “If every new car sold in the world in 2035 were electric, oil demand in 2050 would still be 85m b/d. That is the same as it was in 2010.”

While the shift to electrification is huge, as fossil fuel-based energy is being replaced with electricity, most of the world’s oil is and will be used for industrial processes, such as manufacturing and chemical production, along with heavy-duty transportation such as shipping, trucking, and aviation. This is especially true for future economic growth in the developing world. Within that composition, oil demand plateaus beyond 2030 and remains above 100m b/d even in 2050.

Petroleum Economist does not see oil demand peaking in the next 15–20 years. In this regard, we are closer to the OPEC view, which perceives this long-term reality in a business-as-usual scenario. Global demand for oil will continuing to grow through to 2040 before plateauing at around 125m b/d by 2050, from 102.2m b/d in 2023. India will account for 9m b/d of growth, or close to a third of the non-OECD total, with China contributing just 3m b/d as its economy matures and transitions towards services and electric vehicles.

Supply from present sources will naturally decline at a rate above 10% per annum if upstream investment drops to zero and no oil is extracted from new fields. This is especially true due to the shift towards unconventional sources of oil and gas. These are mostly shale and dense rock formations where production typically declines faster.

Petroleum Economist is not alone in this regard. Without no new investment, we see global oil supplies falling by more than 10m b/d in one year if upstream investments cease to exist. At that rate, by 2030, oil supplies would fall from 100m b/d to less than 50m b/d—that is 50m b/d short of what is needed to meet demand every day. Given price responses to past oil supply shocks, the permanent loss of 10% of oil supply per year could raise prices exponentially. Prices rose 200% during the oil price shocks of the 1970s. Without investment in new oil and gas developments, there are huge risks of energy shortages.

We applaud OPEC for pointing out that $17.5t in oil investment will be needed by 2050, or around $640b/yr on average, of which $14.2t—or 81%—will need to be directed towards the upstream. This seems a hard dose of reality to avoid price shocks and global economic damage whatever may be the risk to climate.

In contrast, if the present trend continues and the world continues to invest, global liquids supply should rise to 122m b/d by 2050 from 102m b/d in 2023—even with the right investments falling just about shy of demand. At least two-thirds of this 20m b/d increase will likely come from countries that today make up OPEC+, which should mean the alliance maintains effective management of the oil market for long into the future if it can manage its internal divisions.

Supply from outside the OPEC+ is forecast to rise dramatically to 59m b/d by 2030, from 51.7m b/d in 2023, but then begin to edge lower from the early 2030s to 57.3m b/d by 2050, due to declining US production. OPEC sees US output peaking at around 23m b/d in 2030, before plateauing and declining slowly to 19.4m b/d by 2050.

Gas

Petroleum Economist sees global gas demand increasing by more than a third, reaching 5.5tcm by 2050. This forecast aligns with the Gas Exporting Countries Forum’s view. Asia-Pacific will account for at least half of global net demand growth, and Africa’s consumption is set to grow at the fastest rate globally. In Europe, gas demand is anticipated to decline from 463bcm in 2023 to below 300bcm by 2050, due to energy policies and deindustrialisation.

Power generation remains the primary driver of demand growth, accounting for some 40% of the total increase. Gas demand for hydrogen production, encompassing both blue and grey hydrogen, is projected to increase from 259bcm in 2023 to 500bcm by 2050.

Global gas production is projected to reach similar levels to demand, with North America expected to remain the world's largest producer by region, reaching 1.5tcm by 2050. The Middle East is projected to experience significant growth, with production rising to 1.2tcm by 2050 and its share increasing to more than 20% from 17% in 2023.

The Middle East will account for the largest incremental gas production growth in the forecast period, while Africa is the fastest-growing region.

To read part one of our energy outlook, click here. To read part three, click here.

Comments